The Somali central bank today licenses fifteen commercial banks, fourteen domestic and one foreign, alongside a newly regulated tier of microfinance institutions. A country that had no formal banking sector at all now has a small but functioning one, built almost entirely by private entrepreneurs. That is a genuine achievement, and it is worth stating plainly before turning to everything that remains unfinished. It is a sector that has done the easy part of a hard job, and now faces the difficult part.

The difficult part

The Somali central bank today licenses fifteen commercial banks, fourteen domestic and one foreign, alongside a newly regulated tier of microfinance institutions. A country that had no formal banking sector at all now has a small but functioning one, built almost entirely by private entrepreneurs rather than the state. That is a genuine achievement, and it is worth stating plainly before turning to everything that remains unfinished, because the story of Somali banking is neither the triumph its boosters describe nor the basket case its reputation suggests. It is a sector that has done the easy part of a hard job, and now faces the difficult part.

The hard part

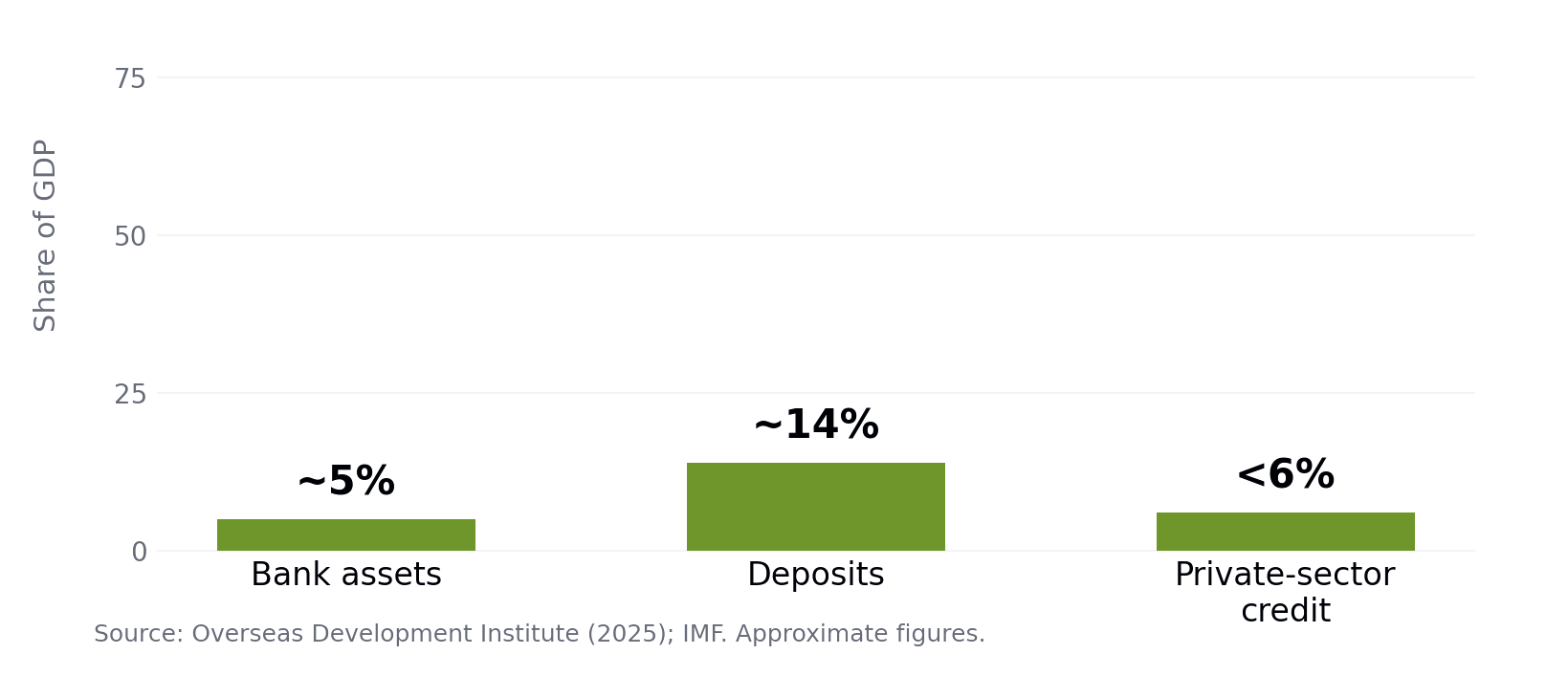

The clearest measure of how small the Somali banking system is the ratio of bank assets to GDP. In a mature economy it runs well above 100 percent; in many low-income African economies it sits between 30 and 50 percent. In Somalia, according to a December 2025 analysis by the Overseas Development Institute, bank assets amount to roughly 5 percent of GDP, with deposits at about 14 percent. The formal banking sector, in other words, touches only a thin slice of the economy.

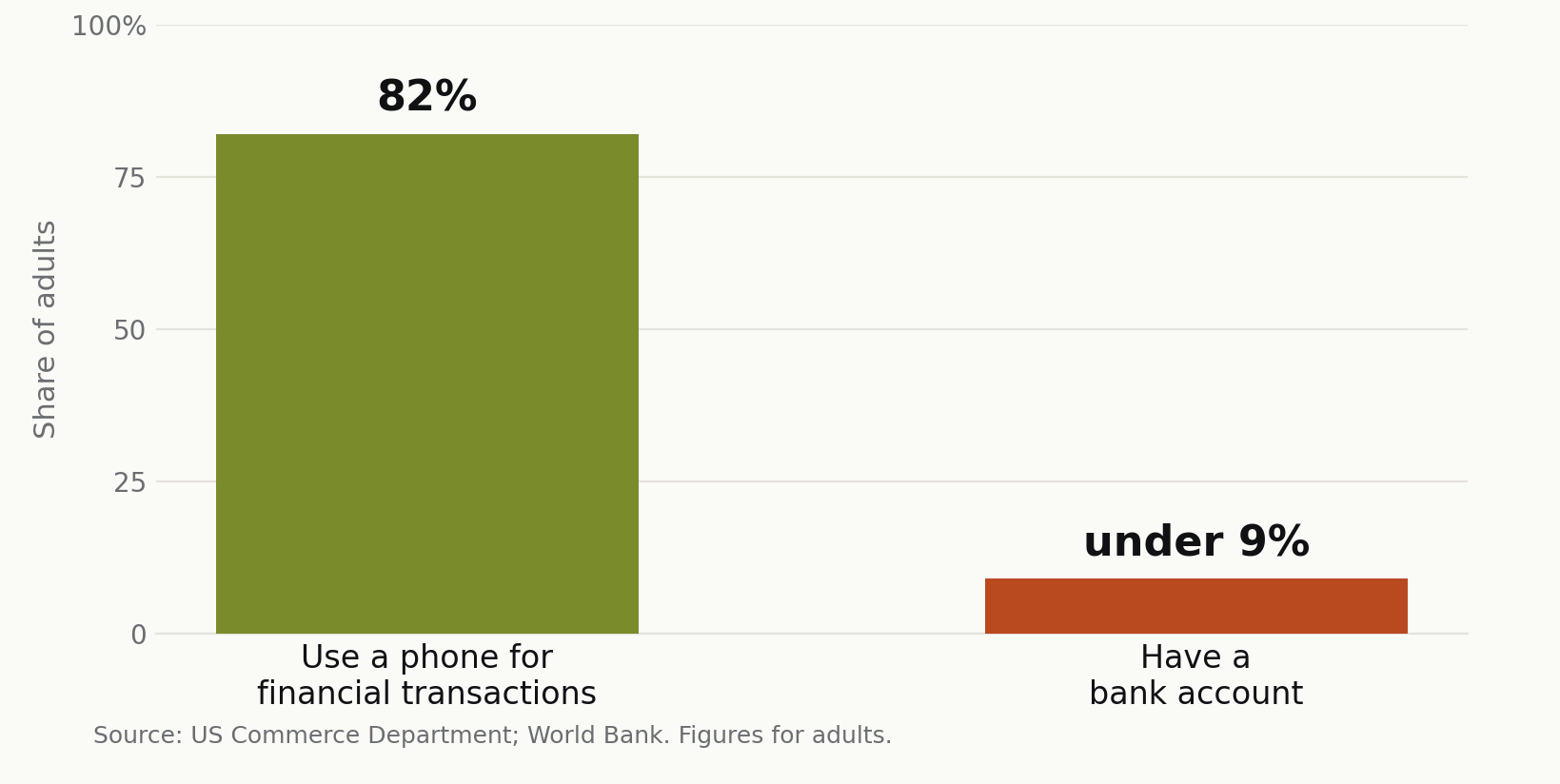

The same picture appears when measured by people rather than money. By the figures in the official commercial guidance on Somalia, fewer than 9 percent of adults have a bank account, and access is concentrated in the cities; in the nomadic, herding economy that still supports much of the population, banks are almost entirely absent. The same analysis finds that total bank assets grew by about 17 percent between 2018 and 2024, modest growth. A formal banking sector that reaches under a tenth of adults is, by definition, not the main way most Somalis hold or move money.

The paradox at the centre of Somali finance

Somalia also has one of the world's smallest formal banking sectors sitting directly on top of one of its most advanced mobile-money economies. Mobile money is not a niche in Somalia; it is the main way money moves. By the World Bank's count, the country records around 155 million mobile-money transactions a month, worth USD 2.7 billion, equivalent to roughly 36 percent of GDP every month, the bulk of it through services such as Hormuud Telecom's EVC Plus. The contrast with formal banking is stark: against fewer than 9 percent of adults with a bank account, 82 percent use a phone for financial transactions.

Somalis, in overwhelming numbers, bank by phone rather than at a bank. This is not a recent development. As far back as 2014, the World Bank's Global Findex survey found that around 35 percent of Somali adults already had a mobile money account, among the highest rates in the world at the time and second in the region only to Kenya. Somalia has at this point been a mobile-money society for more than a decade, well before its current formal banks had been built.

The diaspora's remittances run along the same rails. Somalia's National Bureau of Statistics, in its 2022 Integrated Household Budget Survey, the first such survey since 1985, found that nearly one in five households receives remittances from someone outside the household, and that those transfers arrive mainly through hawala money-transfer operators and mobile money rather than through banks. The roughly USD 2 billion a year that the diaspora sends home, a sum equivalent to around 30 percent of GDP, largely bypasses the banking system entirely.

The significance of this is easy to miss. In most countries the payments system sits on top of the banking system: you pay through your bank, even when it does not feel like it. Australia's PayID and Sweden's Swish, two of the most seamless instant-payment networks in the world, were both built by the established banks and run on shared bank-owned infrastructure; every transfer ultimately moves between bank accounts. Somalia inverted that order. It built a fast, near-universal digital payments network without first building the banks underneath it, and the firms that run it are not banks but telecoms. Hormuud, Golis and Telesom provide what amounts to quasi-banking, deposit-like balances, transfers and credit, without operating under the full prudential rules a licensed bank must follow. The result, as the Overseas Development Institute puts it, embeds concentration risk, regulatory gaps and weak oversight. A handful of firms hold an enormous share of the country's everyday money, and if one falters, the disruption would be national.

Why Somali banks are fragile

Beneath the modest growth of Somali banking lie four structural weaknesses, each of which compounds the others.

The first is dollarisation. After the Somali shilling collapsed in the 1990s, the US dollar became the currency of daily life and has remained so. The extent is striking: there are effectively no bank deposits denominated in Somali shillings, against roughly USD 1.2 billion in hard-currency deposits and a similar sum held in mobile-money wallets. The Central Bank of Somalia has not issued a banknote since 1991; the shillings still changing hands in Somali markets are pre-1991 notes or, in large part, counterfeits printed by private actors over the years of state absence. A central bank that cannot issue the currency its economy actually uses has almost no monetary policy to speak of. It can steer neither interest rates nor the money supply in any meaningful way, and it cannot act as a lender of last resort, because it cannot print the dollars its banks would need.

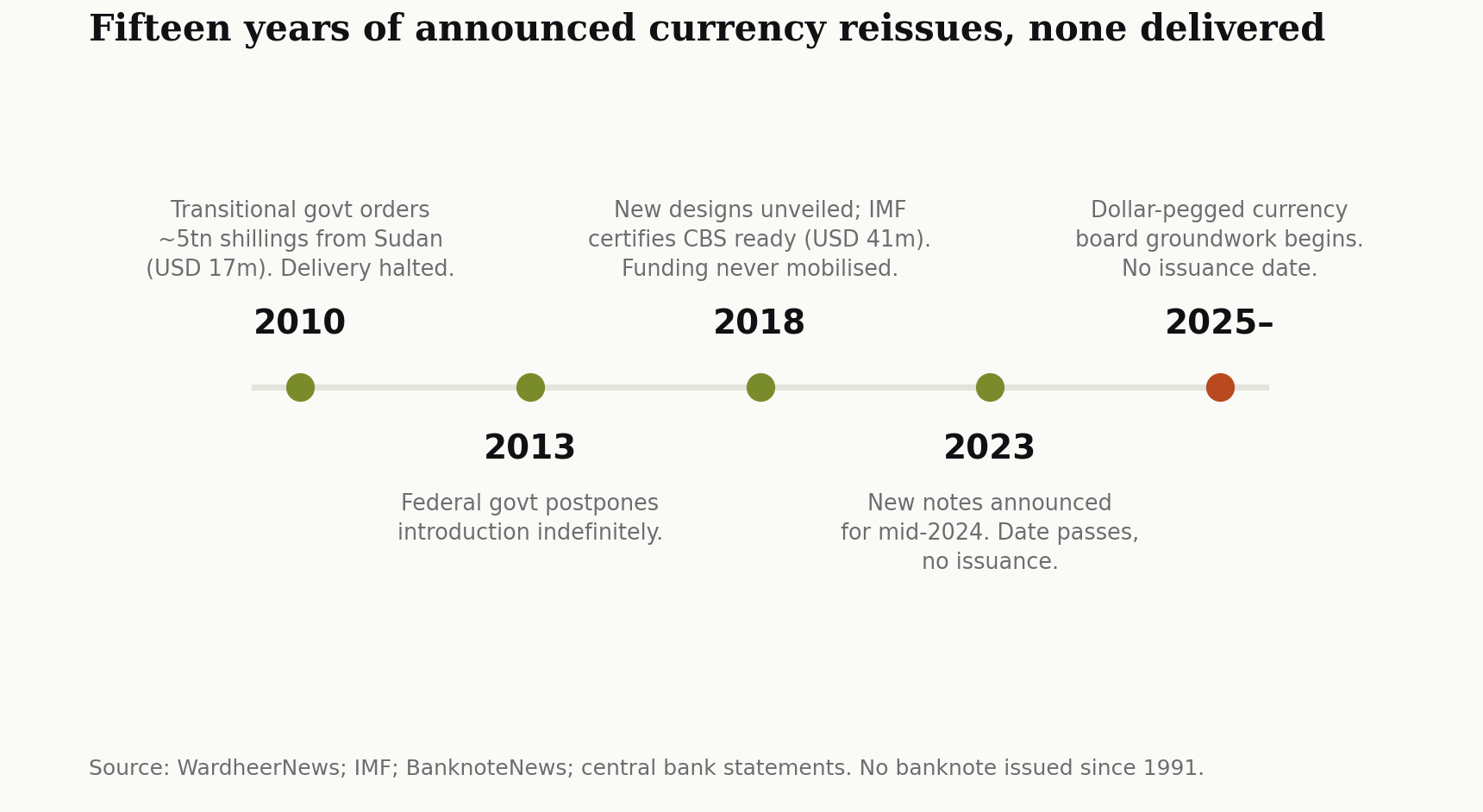

Reissuing the shilling has been an aspiration of every Somali government for fifteen years, and none has achieved it. In 2010 the Transitional Government ordered around five trillion shillings printed in Sudan at a cost of some USD 17 million; the delivery was halted amid opposition. By 2013 the federal government had postponed the introduction indefinitely. In 2018 the finance ministry unveiled new banknote designs and the IMF certified the central bank ready for a first phase of reform, exchanging counterfeit notes, at an estimated cost of USD 41 million; the money was not mobilised and the notes were never issued. In 2023 the central bank announced new banknotes for mid-2024; that date too passed without an issuance.

Each attempt has foundered on the same two obstacles: the funding, which has always depended on donors, and the politics, since the federal government does not control all of the country's territory, the northern regions operate their own currency and monetary authority, and a national shilling cannot circulate where the state's writ does not run, including areas held by the armed terrorist group al-Shabaab. The current effort, structured around a dollar-pegged currency board arrangement under the IMF program, is the most institutionally serious yet, but it carries no issuance date, and the history counsels caution.

The second weakness follows directly from the first. A functioning system has two backstops against a bank failing: a lender of last resort, the central bank lending against good collateral to a solvent bank caught in a temporary liquidity squeeze, and deposit insurance, a guarantee that small depositors are made whole even if a bank goes under. Both exist to break the logic of a bank run, the rational incentive to pull your money first when you fear others will, by removing the reason to run in the first place. Somalia has neither in any robust form, and dollarisation is part of why. A lender of last resort works by creating money to lend; a central bank that cannot issue the currency its banks hold, US dollars, cannot perform the function on demand, because it can only lend dollars it already has. It has no printing press for the money that matters.

The consequence is that depositor confidence rests entirely on the standing of each individual bank, rather than on any system-wide safety net behind it. That makes trust both load-bearing and fragile. In a system with backstops, a solvent bank can withstand a sudden rush of withdrawals because the public knows the central bank stands behind it; in Somalia, a solvent bank facing the same rush has only its own cash on hand, and if that runs out it fails.

The third weakness is shallow credit. Somali banks barely lend. Private-sector credit remains below 6 percent of GDP, and though it is growing quickly, by nearly 23 percent year-on-year in early 2025, it does so from so small a base that the banking system still plays almost no role in financing the wider economy. The household picture is starker: only around a quarter of households have any loan at all, and of those just 2 percent borrowed from a bank, the rest from merchants, traders and personal networks. Lending is held back by the difficulty of enforcing contracts and seizing collateral in a weak legal system, by the Islamic finance frameworks under which most Somali banks operate, and by a shortage of safe assets to deploy into. The Overseas Development Institute notes that even where banks hold liquid assets, deploying them efficiently is difficult for want of investment channels. A banking sector that cannot lend at scale cannot drive growth.

The fourth weakness is fragmentation, which has been the subject of intensive debate. Fifteen licensed banks may sound like a sign of health, but for an economy this small it may amount to too many weak institutions and not enough strong ones. In early 2026, Mohamed Ibrahim, a Somali finance executive and former government adviser, argued that the sector is dangerously fragmented, with no tier-1 institution large enough to anchor systemic stability or underwrite major projects, and that consolidation, merging the many weak banks into a few strong ones, has become essential rather than optional. Larger banks could more easily meet capital requirements, absorb shocks, invest in technology, and win and sustain the correspondent relationships that connect Somalia to the outside world. The central bank's USD 5 million minimum capital requirement is already, in effect, a gentle push toward consolidation, raising the bar a bank must clear to stay in business, and further tightening over time would push in the same direction.

Cut off from the outside

Another significant constraint is also external: whether Somali banks can reach the global financial system at all. To move money across a border, a bank needs access to SWIFT and a correspondent relationship, a foreign bank willing to hold an account for it and clear its transactions. Without a foreign bank willing to stand on the other side, a Somali bank cannot send or receive an international payment, however sound it is at home.

These relationships are scarce in Somalia, and concentrated in a few banks. The International Bank of Somalia is one, and alleges it was the first in the country to implement SWIFT with an international account number. IBS also describes itself as holding the widest network of correspondent relationships in Somalia, and was one of only two Somali banks selected by the International Finance Corporation, the World Bank's private-sector arm, for a trade-finance credit line. Ziraat Katılım is a different case again: its Mogadishu operation is not a separate Somali company but a direct branch of the Turkish state bank, opened in 2023 and backed by the correspondent network of one of Turkey's largest banking groups. Beyond these, the public record thins, and the reasonable conclusion is that cross-border connectivity reaches a handful of banks rather than the sector as a whole.

What sustains this isolation is not any blockade or sanction, but the caution of foreign banks themselves. Over the past decade they have steadily exited relationships they judge too risky to be worth the compliance cost, a practice known as de-risking, and Somalia has been one of the sharpest cases. The US Treasury's own de-risking strategy records that American banks closed the accounts of Somali-American money-transfer firms after the 2012 famine, wary of exposure to designated terrorist groups operating in Somalia and of the weakness of the country's financial oversight. The threat is credible and longstanding: the armed terrorist group al-Shabaab moves money through remittances, banks, cash and mobile money alike. A foreign bank weighing whether to serve a Somali counterpart sees that risk first, and for most the cautious answer has been to stay away.

It is worth being clear here: Somalia is not formally blacklisted. It appears neither on the Financial Action Task Force's lists of deficient jurisdictions nor on the EU's list of high-risk third countries. For decades that absence reflected not a clean record but the fact that Somalia had never been assessed at all. The risk ahead is that when it is, a country with a high terrorist-financing threat and a young compliance regime could still score poorly enough to face increased monitoring, the grey list, formalising the exclusion that de-risking already imposes informally.

What is being built to fix it

None of this is static. Since 2009 the Central Bank of Somalia has been assembling, albeit slowly, the institutional machinery a banking system needs.

It has issued a body of banking regulations and shifted supervision toward a risk-based approach, concentrating scrutiny on the institutions and activities most likely to fail and allowing it to intervene before a problem spreads rather than after. In May 2025 a new Financial Institutions Law rebuilt the legal foundation for licensing and oversight; under it the central bank re-licensed eleven commercial banks in December 2025, in effect re-vetting the sector against tougher standards, and granted the first-ever licences to microfinance institutions a month earlier. Licensing the microfinance institutions matters because it has the potential to bring small-scale lending to more than 70 percent of Somalis outside the banking system.

The most visible change is in payments. Building on the National Payment System it launched in 2021, the central bank in January 2025 introduced the Somalia Instant Payment System, a national switch that lets banks and mobile-money operators settle transfers between each other in real time. Its significance is interoperability: until now a customer of one mobile-money service or bank could not easily pay a customer of another, leaving the country's money penned into separate networks. A shared switch breaks down those barriers, and just as importantly it routes the payment system through supervised, central-bank-operated rails rather than the private networks of the telecom operators, a first step toward bringing those operators under firmer prudential control. Alongside it, the central bank has inaugurated a Financial Stability Committee that brings banks, money-transfer businesses, mobile-money issuers and payment operators under one coordinating body, charged with spotting system-wide risks early, an explicit attempt to get ahead of the concentration risk the large payment actors represent.

Hardest of all, the central bank has begun the groundwork for reintroducing the shilling under a dollar-pegged currency board, the one reform that should strike at dollarisation itself. As the long record of failed attempts shows, that remains the most uncertain of these efforts, yet it is also the only one that addresses the system's deepest constraint at its root.