On 26 June, China's central bank authorised two lenders, South Africa's Standard Bank and the Industrial and Commercial Bank of China, to clear renminbi across Africa, giving African businesses and banks direct access to China's onshore financial system for the first time.

The measure was presented as a technical convenience: cheaper trade settlement, a way for African banks to move money to and from China without routing payments through Western intermediaries, one more step in Beijing’s stated ambition to make the yuan a global settlement currency. That much is true. But the spread of the yuan across Africa is neither the simple modernisation its promoters describe nor the conspiracy its critics fear. It is, for the most part, a debt story. And for Somalia, a country that has just spent years undergoing debt relief, it is the most instructive story on the continent

African Debts Crisis

In 2026, there are twenty-two low-income countries in sub-Saharan Africa who are in or at high risk of debt distress, the World Bank's term for a state that can no longer service its borrowing on the original terms. Public debt across the continent has passed USD 1.8 trillion, having grown since 2010 at roughly four times the pace of economic output. In a rising number of countries the money spent servicing debt now exceeds the money spent on health or education. The largest single bilateral creditor behind this is China, which has lent African governments more than USD 800 billion over two decades.

This is the setting in which the yuan is advancing. The governments embracing it most readily are not doing so out of monetary ambition. They are doing so because they are in trouble, and because the currency offers a way to make their debts, many of them owed to China, a little easier to carry.

Reading the Kenya deal

Kenya is one such case. The nation recently converted three Chinese loans for its Standard Gauge Railway from dollars into renminbi, winning longer repayment terms and fresh grace periods, and cutting its annual debt-service bill by around USD 215 million. But the saving did not come from the currency. It came from the longer maturities and the deferred payments. China agreed to soften the terms, and used the moment to move the loan into yuan. It is no secret that the railway those loans built has struggled to earn enough to cover even its operating costs, let alone repay the debt that financed it. Kenya had borrowed in a foreign currency to build an asset that earns Kenyan shillings, and then could not generate the foreign currency to service the loan. Borrowing in a hard currency to build things that earn only local currency, or earn nothing at all, is what turns lofty infrastructure plans into costly debt with hundreds of millions of dollars going into interest payment alone.

Ethiopia is reportedly also interested in a Kenya-style arrangement, and is presented as the next in line, though that deserves caution. The nation owes some USD 30 billion, a debt the IMF judges unsustainable. It defaulted on its sole Eurobond in late 2023 and has still not reached agreement with its private bondholders, even as it restructures around USD 15 billion of external debt with its official creditors. AidData, the research group at the College of William and Mary that tracks Chinese lending, estimates Ethiopia could save as much as USD 778 million through a Kenya-style conversion. But that is a projection, not a deal that has been struck, and the same researchers caution against assuming it will happen. Some of Ethiopia’s railway loans to China were already restructured once before, in 2018, when Beijing extended the repayment term on the Addis Ababa to Djibouti line from ten years to twenty. A borrower that has been to the table before, and is again in default, is not an obvious candidate for fresh concessions. The conversions now being discussed are best understood as moments within a long-running debt crisis, not a strategy any government would choose from strength.

What the relief conceals

The China's Export-Import Bank is also increasingly encouraging, and in some cases requiring, borrowers to take new loans in yuan rather than dollars. Zambia, the first African country to default this decade and still entangled in restructuring years later, counts China as its largest bilateral creditor.

It is here a pattern emerges; Debt-distressed African governments get cash-flow relief while china gets its currency lodged deeper in the continent's sovereign balance sheets, advanced through the very institutions that hold the debt. The conclusion here is that the yuan is not winning Africa in the open market so much as through the loan book.

Converting debt into yuan also carries its own potential drawbacks. As some institutions warns, a government that converts its debt to yuan still has to find yuan to repay it. If its own currency weakens against the renminbi, the saving erodes. The reason is currency risk: the African governments earn revenue in local currency but must buy yuan to repay a yuan loan, so when the local currency falls, each unit of yuan costs more and more revenue goes to servicing the same debt. A large enough depreciation cancels the lower interest rate altogether. The borrower has then traded a cheaper coupon for exchange-rate exposure, and against a currency whose convertibility Beijing controls.

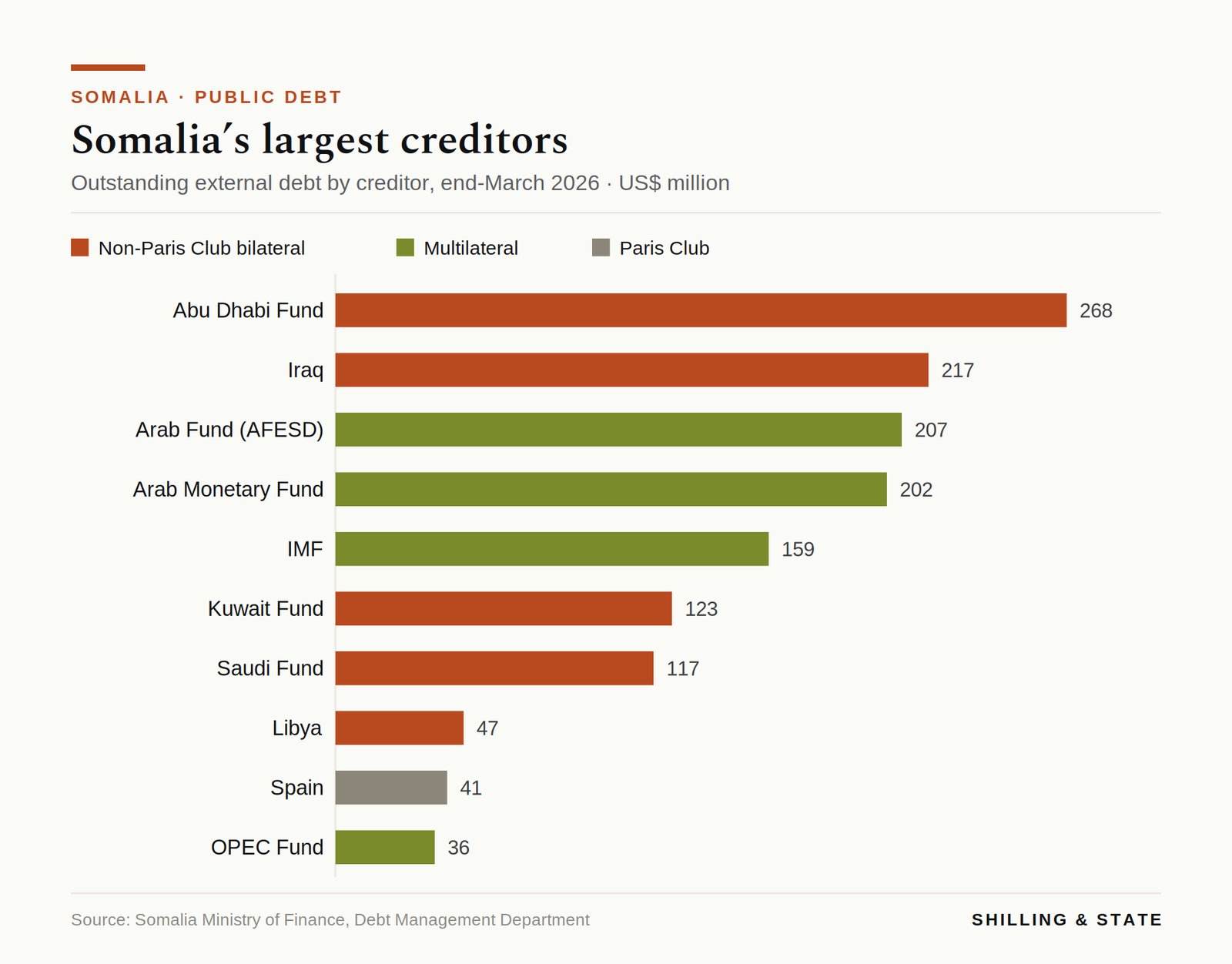

Somalia’s unusual position

It must be noted that here Somalia stands almost alone. Having completed the Heavily Indebted Poor Countries process, the multilateral mechanism that cancelled the arrears of the world’s poorest and most indebted states, it now carries external debt of around USD 1.5 billion, close to 8 percent of output, far below its neighbours. More striking is that Somalia’s borrowing is owed to multilateral institutions and to Arab bilateral lenders, and none of it to Beijing. Where the rest of the continent approaches the yuan from distress, and often from debts owed to China, Somalia would approach it, if it ever did, from a clean slate. That is a rare and valuable position, and one the federal government must recognise before it considers to eventually borrow again.

The lesson for Somalia is not that the yuan is dangerous and the dollar safe, or the reverse. It is that debt itself, in any foreign currency, is the thing to be governed with discipline and transparency. Three principles follow from the continent’s experience with debt.

The first is that foreign debt should fund assets that generate a return, and the honest test of an asset is whether it produces the revenue to service its own loan. A road, a ministry building or a prestige project that earns nothing is not a candidate for a Eurobond or a Chinese loan. The loan still has to be repaid, and a non-earning asset simply shifts that burden onto the general budget. It is a path to future restructuring.

The second is to match the currency to the cash flow. Borrowing in dollars or yuan to build something that earns Somali shillings is the precise trap that caught Kenya, and converting between currencies later does not undo it.

Foreign-currency debt belongs only against projects that themselves earn foreign currency, such as an export terminal or a port that handles international trade. Everything else should be financed at home, or through grants and concessional borrowing. Public-private partnerships can have a place, but only where the private partner carries genuine risk; structured loosely, they become hidden debt by another name, and eventually a state obligation that does not appear on the books until the project fails.

The third is to set a hard ceiling, and here the gap is subtle. Somalia already has much of the architecture. The 2019 Public Finance Management Act governs how the state contracts debt, and under its IMF programme the country has held to firm limits on new borrowing for years. But those limits are largely programme conditions, renegotiated at each review and dependent on the Fund’s continued presence. They discipline the government only as long as it wants the Fund’s money. What Somalia lacks is a permanent statutory cap, written into its own law and measured against output and revenue, that binds even after the programme ends. That is the moment of real danger: a state fresh from debt relief, newly creditworthy, with access to lenders, and no longer under the Fund’s eye. A country that legislates its own ceiling now, while the discipline is still in place, is one that cannot quietly abandon it later. Every country now in distress arrived there one reasonable-sounding loan at a time, and a binding limit is the only thing that halts that progression, because the individual deals almost always make sense in isolation.

None of this means refusing the world’s capital. Sound public finances are what eventually earn a country access to markets on fair terms in the first place. However, the governments now converting their dollars into yuan are not a model to emulate but a map of where the easy road leads. The discipline now is to stay on the harder one.