New reforms would force Somali lenders to recognise loans that fall behind and cap how much they can lend to a single borrower.

The Central Bank of Somalia is preparing to overhaul the rules governing how banks account for problem loans, in a reform developed with the International Monetary Fund that would for the first time require lenders to set money aside against credit that falls even a day behind.

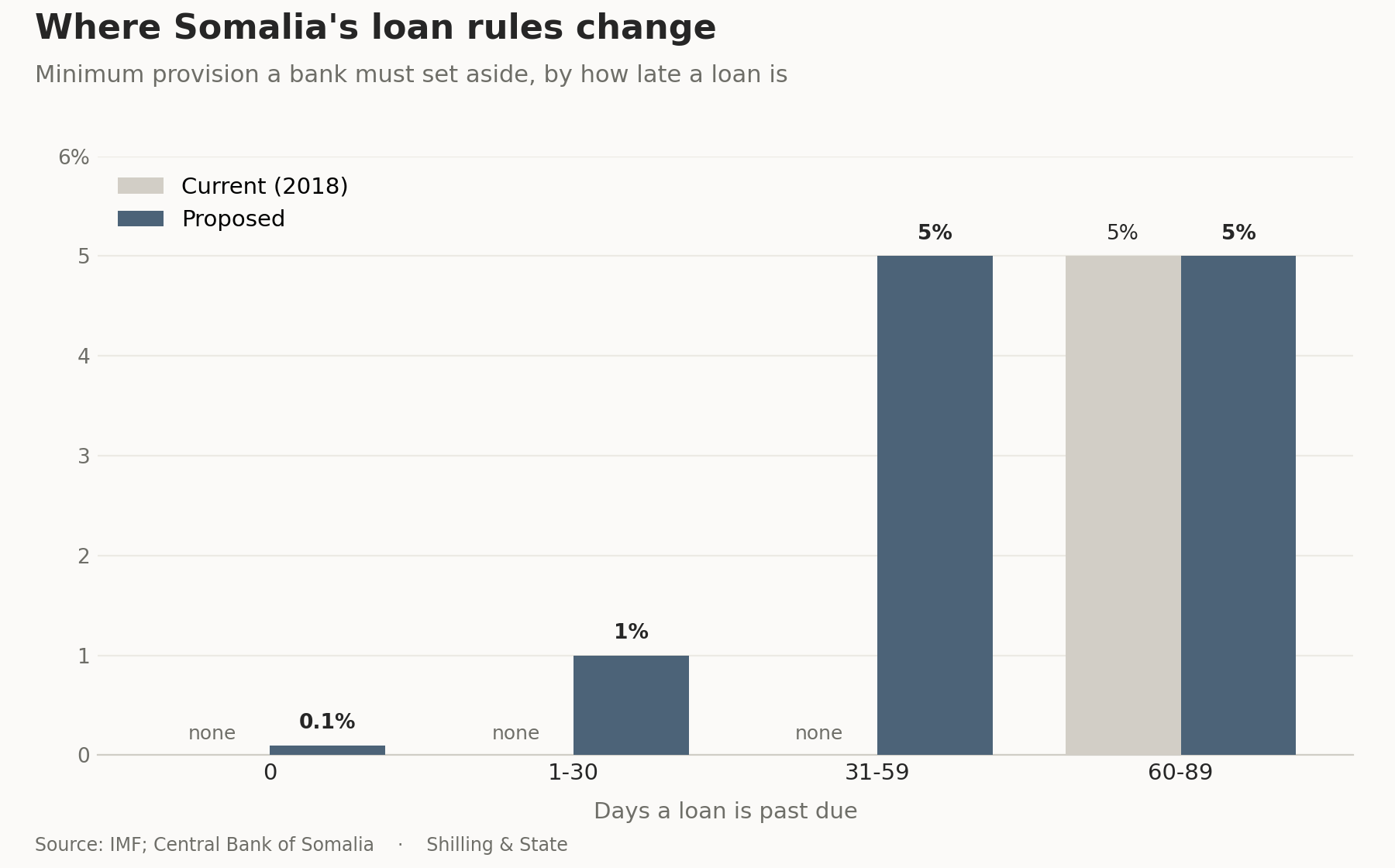

The proposed regime would also cap how much a bank can lend to any single borrower and give the central bank explicit powers to penalise those that break the rules. It would be the first substantial revision of a framework written in 2018, which the IMF found treats too many loans as sound and leaves banks with little reason to flag borrowers who have begun to fall behind.

Much of the weakness stems from the structure of Islamic banking, under which Somali lenders cannot charge interest on overdue payments or keep penalties for late repayment. In practice, the IMF found, banks write no late-payment penalty into their contracts at all, leaving borrowers with little incentive to keep to schedule. A loan can run weeks past due while still recorded on the books as healthy.

To close that gap, the reform introduces a category for loans between one and 30 days late and requires banks to provision against them, at a proposed 1 per cent. Loans that are fully up to date would carry a charge of 0.1 per cent. The sums are small; the intent is to stop banks treating a loan as risk-free merely because no interest has been charged on it. The change raises the number of loan classifications from five to six and aligns the thresholds with international accounting and supervisory standards.

The revision also confronts a reliance on losses that have already materialised. Somali banks tend to wait until a loan has clearly soured before recognising the risk, the IMF said, rather than providing for losses they can anticipate. Under the new rules, banks must hold provisions against expected losses across the entire loan book, calculate them on a loan's full value without deducting collateral, and reclassify a customer's other loans once any one of them turns bad.

Separately, the reform caps lending to a single borrower at 25 per cent of a bank's core capital, the first binding limit of its kind in Somalia. The existing rules flag large exposures for reporting once they exceed 10 per cent of capital but set no ceiling on them. The cap, proposed by the central bank itself, addresses a danger common to small banking systems, where the failure of one dominant borrower can imperil a lender. Its bite will depend on how concentrated Somali banks' lending already is, which the central bank does not disclose.

Banks would also report more frequently to the central bank, which would gain explicit authority to sanction those that breach the rules, mirroring its powers over capital and liquidity. The emphasis reflects a recurring finding in the central bank's own inspections: that weak governance, more than any individual bad loan, poses the greater threat to banks' soundness.

The rules are not yet final. The central bank must assess how the new categories would reshape banks' balance sheets and consult lenders before fixing the detail, and a date for the regime to take effect.