A new interest-free financing plan from Hormuud Telecom and Get-Phone lets low-income Somalis buy their first smartphones in small daily instalments, on better terms than similar schemes elsewhere in East Africa. For Hormuud, it opens a new line of business built on infrastructure it already owns.

Somalia's largest telecommunications company wants to put an internet-ready phone in every hand it can reach, and it has built a way for customers to pay for it a few cents at a time. In early May, Hormuud Telecom announced in Mogadishu a partnership with Get-Phone, a local device-financing firm, to sell smartphones on credit to people who have never been able to afford one.

Although 4G now reaches more than 70% of a population of around 19 million, about half of Hormuud's own customers still use 2G or basic feature phones, by the company's account. A customer puts down a deposit of about $19 and then pays between $0.60 and $1.60 a day, depending on whether the plan runs for six, nine or twelve months, according to Hormuud and Get-Phone. The daily charge covers both the device instalment and a bundle of 1GB of data and 40 minutes of calls. Because the average Hormuud customer already spends around $0.50 a day on data and voice, the cheapest plan adds a financed smartphone for roughly 10 cents more a day. Repayments run through EVC Plus, Hormuud's mobile-money platform, and three entry-level ZTE handsets are on offer. Get-Phone says the financing is Sharia-compliant and charges no interest.

Eligibility does not hinge on a bank account or a credit history, neither of which most Somalis have. Instead Hormuud scores applicants on information only it holds: how long they have kept a SIM card active and how they use their mobile money. Approved customers are then sorted into risk tiers and matched to a device and a repayment plan. A pilot in Mogadishu between February and March produced a default rate below 4%, the companies said, helped by a feature that let customers stand as guarantors for relatives, including family in rural and nomadic areas. Miss a payment and access is paused rather than penalised, with the missed days added to the end of the term. The first phase aims to place 10,000 devices by June, a target now falling due, with 100,000 planned by the end of the year as the scheme extends from central and southern Somalia into Puntland and the northwest. Somalia's deputy prime minister, Salah Ahmed Jama, appeared at the launch to call the smartphone a gateway to commerce and financial inclusion.

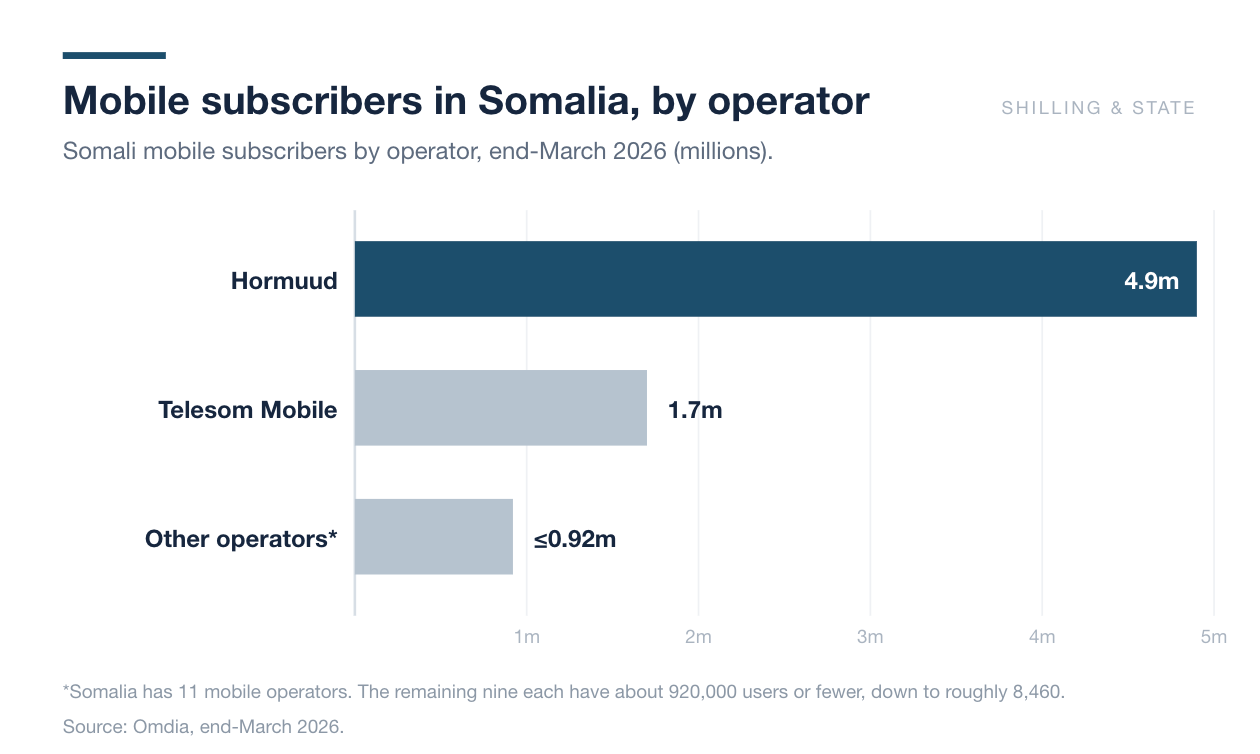

For Hormuud, the programme is a natural extension of an integrated business it has built over two decades. The company already provides the network the devices run on and the mobile-money platform through which they are repaid, and its own credit assessment now allows it to offer financing as well. Because it supplies the handset, the connection, the data and the credit together, it can package them at a price few standalone providers could match, and it can gauge creditworthiness from the SIM history and mobile-money activity it already holds, extending credit to customers who have neither a bank account nor a formal credit record. The scale behind that reach is considerable: by the count of the research company Omdia, Hormuud has close to 5 million mobile users and is the largest of Somalia's eleven operators. The scheme opens a new line of revenue, strengthens ties with existing customers, and moves more of them onto the higher-value data services its network was built to carry.

None of this was invented from scratch. Device financing repaid in small mobile-money instalments is the model Kenya's Safaricom built into Lipa Mdogo Mdogo and that M-KOPA has spread across several African markets, each turning a modest deposit and a daily charge into mass smartphone ownership. What Somalia has borrowed it has also adjusted. The Kenyan schemes charge interest and have drawn years of complaint that customers end up paying well above a handset's cash price, to the point that lawmakers there have debated bringing device financing under central-bank supervision. By making its offer interest-free and Sharia-compliant, the Somali version steps around the criticism that has followed the original, and on the consumer's own terms it is the better deal.