At the end of the first quarter of 2026, Somalia’s public debt stood at $1.47bn, all of it external. The stock has remained broadly stable as creditors settle arrears under debt-relief agreements, while the government has tightened borrowing rules and kept debt service low. Risks remain contained for now, though repayments are set to rise as grace periods expire.

Debt stock

Somalia’s public debt stood at $1.47bn at the end of March, according to the finance ministry’s first-quarter debt bulletin, with the entire stock made up of external liabilities. The government has yet to issue domestic securities, raise money on the local market or extend sovereign guarantees, leaving its debt profile fully exposed to foreign creditors.

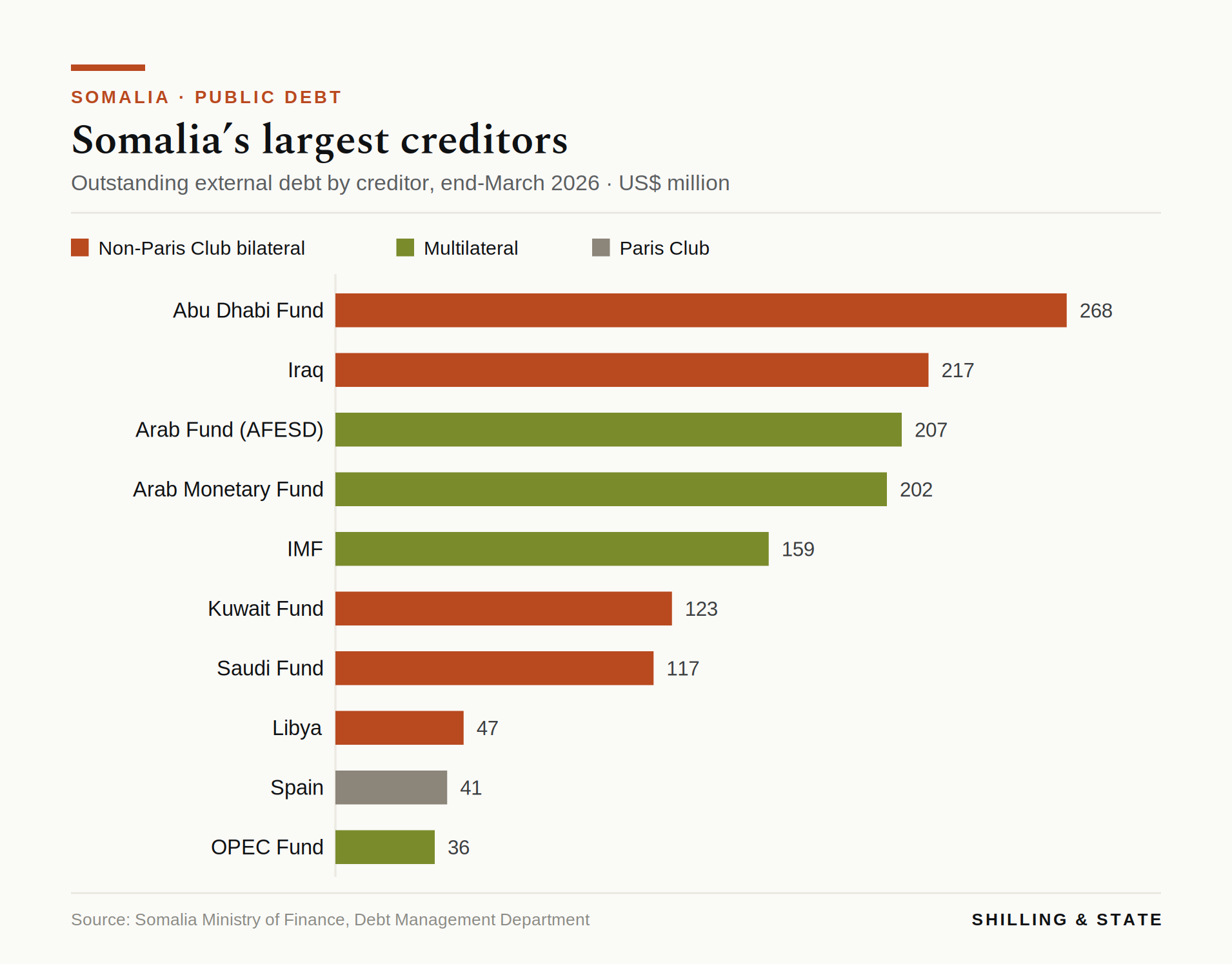

Bilateral lenders account for the largest share of the debt stock, holding $833.1mn, or 57 per cent of the total. Almost all of that sits with non-Paris Club creditors, led by the Abu Dhabi Fund for Development with $267.8mn, followed by Iraq with $217.2mn, the Kuwait Fund with $123.3mn and the Saudi Fund with $116.5mn. Spain, however, remains the only Paris Club creditor with a material outstanding claim, at $40.9mn.

Multilateral lenders, meanwhile, account for the remaining $633.7mn, or 43 per cent of the portfolio, led by the Arab Fund for Economic and Social Development, the Arab Monetary Fund and the IMF. Commercial exposure remains negligible, with a single $2.8mn loan owed to a Serbian company.

Management and arrears

Somalia’s debt stock has changed little over the past year, edging down from $1.48bn at the end of 2025. The more notable shift, however, has been in arrears, which have fallen as creditors implement relief agreed under the Heavily Indebted Poor Countries framework. Outstanding arrears stood at $490mn at the end of the first quarter, equivalent to about 34 per cent of total debt, down from $499mn three months earlier.

The finance ministry concluded a series of restructurings through 2025. The Abu Dhabi Fund, Somalia’s largest single creditor, signed a 40-year restructuring agreement in February 2025, including a 16-year grace period and a suspension of interest payments until the end of 2028. The Arab Monetary Fund followed in April with a 20-year rescheduling at zero interest. Spain, meanwhile, agreed in principle to a debt-for-development swap that would cancel 60 per cent of its claim upfront. Romania agreed to write off 85 per cent of its exposure, while Algeria confirmed full debt forgiveness in February 2026.

Risk profile

Somalia’s debt portfolio carries limited market risk, with almost all liabilities locked in at fixed interest rates. Variable-rate exposure is confined to a small portion owed to non-Paris Club creditors, limiting sensitivity to shifts in global borrowing costs. The average time to maturity stands at around 19 years, while only 1.6 per cent of the debt stock falls due within the next 12 months, keeping refinancing pressures low for now.

The repayment profile, however, becomes heavier from 2027 onwards, as grace periods on restructured loans begin to expire and scheduled payments to Spain and an IMF facility come due.

Currency risk remains the clearest vulnerability. The entire debt stock is denominated in foreign currencies, leaving Somalia exposed to exchange-rate fluctuations. Roughly a quarter of the portfolio is held in UAE dirhams, while close to a fifth is denominated in Kuwaiti dinars and the Arab Monetary Fund’s accounting unit. Smaller portions are held in special drawing rights and Saudi riyals, with about a tenth in US dollars. The IMF continues to assess Somalia as facing a moderate risk of debt distress.

Fiscal stance

Debt service remains modest. Somalia paid $8.1mn to creditors in 2025, equivalent to less than 1 per cent of government revenue, and met all scheduled repayments in the first quarter of 2026 without accumulating new arrears. That burden, however, is expected to rise as grace periods on restructured loans begin to expire.

For now, fiscal policy remains anchored on concessional borrowing. The government’s medium-term debt strategy limits new financing to highly concessional terms, while the fiscal deficit is targeted at 0.2 per cent of GDP this year and capped at 3.5 per cent over the medium term under the IMF-backed programme.

Revenue growth has offered some support. Domestic collections rose 11 per cent in 2024, while an income tax law passed last year is intended to broaden the tax base and reduce reliance on external support.

That support, meanwhile, remains critical. Somalia’s eligibility for grant financing under the World Bank’s IDA framework has been extended until June 2028. After that, concessional loans rather than grants are expected to play a larger role in funding development, increasing the importance of maintaining debt discipline.

Holdout creditors and institutional reform

The government has set out a formal strategy for the creditors that remain, centred on the principle of comparability of treatment. Holdout lenders are expected to accept terms equivalent to the relief granted by Paris Club members, using the Common Reduction Factor established under the HIPC framework to align settlements to a common standard.

Iraq, Libya and the Arab Fund remain among the holdouts, while the ministry has continued follow-up contacts with Bulgaria and Serbia. Iraq’s claim stands out in particular: of its $217mn exposure, only $31mn is principal, with the remainder made up of accumulated interest and fees — the largest such build-up in Somalia’s debt portfolio.

Those negotiations have unfolded alongside a broader institutional rebuild at the finance ministry. The Debt Management Department has been reorganised and the government has begun publishing quarterly debt bulletins, offering a more regular window into the country’s debt profile as it moves deeper into the post-relief period.